Has the Management Body formally approved and remains accountable for the ICT Risk Management Framework?

Has the Management Body formally approved and remains accountable for the ICT Risk Management Framework?

Mandated: Article 5(2); Article 6(1)

Note:

DORA explicitly assigns accountability to the management body for defining, approving and overseeing the ICT risk framework. This is not delegable to IT.

How CUDORA Helps:

Helps develop a structured DORA-aligned ICT Risk Management Framework with board-ready approval documentation and oversight reporting.

Has a documented DORA Gap Assessment been performed across Articles 5–15 and 24–30?

Has a documented DORA Gap Assessment been performed across Articles 5–15 and 24–30?

Mandated: Article 6(1) (well-documented framework requirement)

Note:

Without a structured baseline assessment mapped to DORA Articles, the Board cannot evidence oversight or proportionality.

How CUDORA Helps:

Delivers a comprehensive IT Thematic and DORA gap assessment, mapped directly to regulatory Articles and RTS requirements.

Have Board Members undertaken structured ICT risk training to maintain competence?

Have Board Members undertaken structured ICT risk training to maintain competence?

Mandated: Article 5(4)

Note:

DORA requires management body members to actively maintain sufficient knowledge and skills to understand ICT risk and its impact.

How CUDORA Helps:

Provides access to board-focused DORA training sessions and evidence of competence aligned to Article 5(4).

Has the Board adopted and reviewed a formal ICT Third-Party Risk Strategy?

Has the Board adopted and reviewed a formal ICT Third-Party Risk Strategy?

Mandated: Article 28(2)

Note:

DORA requires a documented strategy on ICT third-party risk — this goes beyond vendor management procedures.

How CUDORA Helps:

Develops a proportionate ICT Third-Party Risk Strategy tailored to credit union outsourcing models.

Do You Maintain a DORA-Compliant Register of Information for ICT Third-Party Providers?

Do You Maintain a DORA-Compliant Register of Information for ICT Third-Party Providers?

Mandated: Article 28(3) + ITS on Register of Information

Note:

DORA requires a structured register in a prescribed format. Informal supplier spreadsheets are unlikely to meet ITS requirements.

How CUDORA Helps:

Supports a structured third-party register aligned to DORA ITS technical specifications.

Can You Classify and Report Major ICT Incidents Using DORA RTS Threshold Criteria?

Can You Classify and Report Major ICT Incidents Using DORA RTS Threshold Criteria?

Mandated: Articles 17–19 + RTS on Incident Classification

Note:

DORA introduces prescriptive classification thresholds and reporting timelines for major ICT-related incidents.

How CUDORA Helps:

Aligns incident management playbooks and ransomware response procedures with DORA RTS criteria.

Do You Operate a Documented Digital Operational Resilience Testing Programme?

Do You Operate a Documented Digital Operational Resilience Testing Programme?

Mandated: Articles 24–27

Note:

DORA requires a structured, documented resilience testing programme — beyond routine vulnerability scans.

How CUDORA Helps:

Designs a proportionate resilience testing programme framework suitable for credit unions.

Have ICT Dependencies Supporting Critical or Important Functions Been Mapped?

Have ICT Dependencies Supporting Critical or Important Functions Been Mapped?

Mandated: Articles 11 & 28

Note:

DORA requires identification of critical functions and their ICT dependencies, particularly where third parties are involved.

How CUDORA Helps:

Facilitates structured mapping of critical services and ICT dependencies with governance oversight reporting.

Is Proportionality Explicitly Documented Within Your ICT Risk Framework?

Is Proportionality Explicitly Documented Within Your ICT Risk Framework?

Mandated: Article 6(1)

Note:

Credit unions benefit from proportionality — but it must be demonstrable and justified within documented frameworks.

How CUDORA Helps:

Ensures proportional implementation is clearly articulated and defensible under supervisory scrutiny.

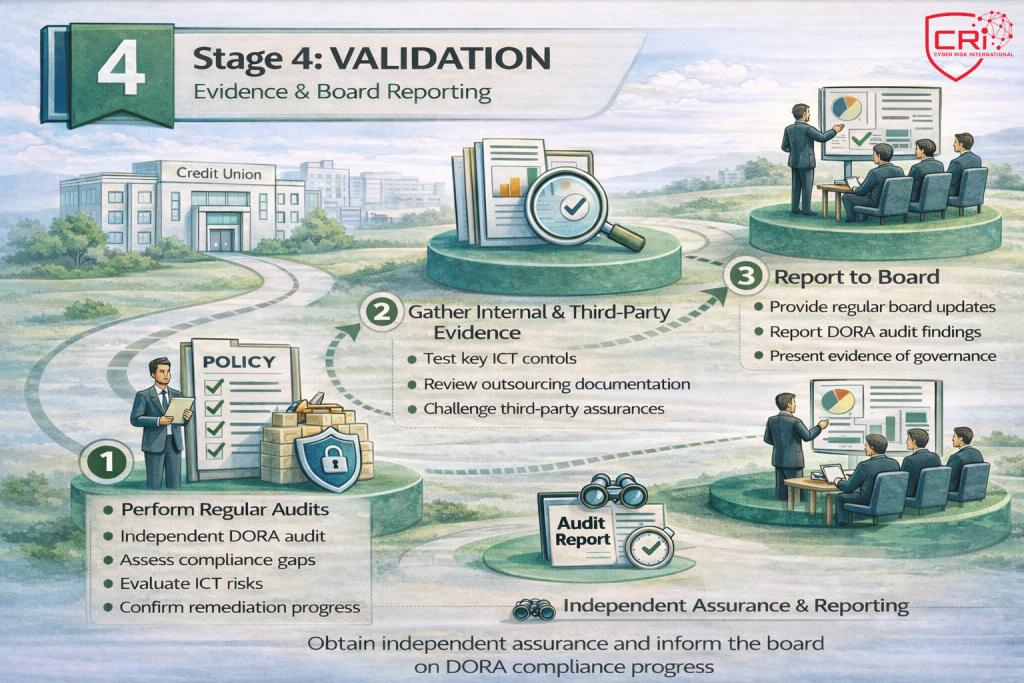

Can the Board Evidence Ongoing Oversight of Digital Operational Resilience?

Can the Board Evidence Ongoing Oversight of Digital Operational Resilience?

Mandated: Article 5(2); Article 6(5)

Note:

Approval is not sufficient. DORA requires ongoing oversight, review and continuous monitoring.

How CUDORA Helps:

Provides structured board reporting dashboards and periodic resilience posture updates.